As it grapples with the COVID-19 pandemic, California faces an uncertain fiscal future. This global crisis has caused a sharp decline in economic activity, exposing crucial sectors to heightened risk. As discussions continue about when and how to re-open the economy, it is clear that the state will have to respond to significant fiscal challenges.

The good news is that California has made important changes to its reserve policies since the Great Recession. The passage of Proposition 2 (2014) created the Budget Stabilization Account—the state’s rainy day fund—as well as the Public School System Stabilization Account, a separate reserve for K–12 districts and community colleges. In addition, Governor Brown and the legislature created the Safety Net Reserve Fund to shore up Medi-Cal and CalWORKs funding during downturns.

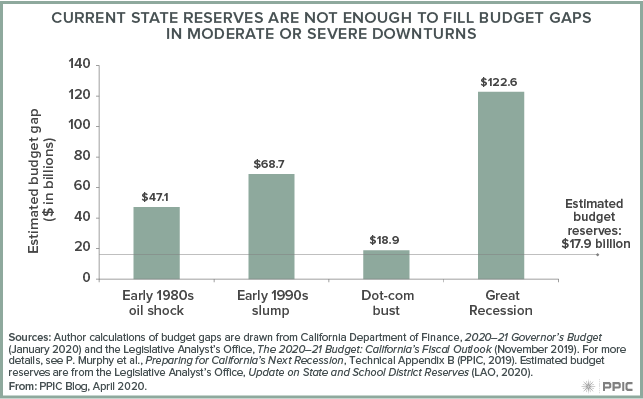

The bad news is that a severe recession is likely to pose significant budgetary challenges. Drawing from the state’s experience during several recent recessions, PPIC estimated the budget ramifications of mild, moderate, and severe recessions and the capacity of state reserves to fill gaps. We found that the state’s reserve balance—estimated to be $17.9 billion—is large enough to withstand a mild recession such as the dot-com bust in the early 2000s.

However, a long and/or severe recession like the early 1980s oil shock (which lasted four years), or the early 1990s slump and the Great Recession—both of which were much more severe and lasted five years—would create large budget gaps and require policymakers to make difficult decisions. (It is important to note that the estimated reserve balance relies on the 2019–20 enacted budget and that it will change when revenue estimates are updated in May.)

In the meantime, the federal government has stepped in. The Families First Coronavirus Response Act includes an increase in the federal share of Medicaid payments and reimbursements to states that are expanding public assistance programs. The Coronavirus Aid, Relief, and Economic Security (CARES) Act provides about $2.2 trillion; some aid goes directly to families, some goes to schools, and some to state and local governments. Additionally, two federal disaster declarations make many of California’s COVID-19 expenditures eligible for at least partial reimbursement.

Governor Newsom has requested additional federal assistance, including flexible aid to state and local governments, a further extension of unemployment insurance benefits, and expanded support for safety net programs, small businesses, K–12 and higher education systems, childcare, and broadband.

The state is also making significant changes to the 2020 budget process. The Department of Finance is drafting a “workload” budget for the May Revision that will set the baseline for the final budget to be enacted in June. This will limit spending increases while allowing for growth in programs—particularly safety net programs—that expect increased demand. The legislature will revisit the budget for an “August Revision” that reflects changes in the state’s financial condition. As these processes move forward, PPIC will continue to monitor California’s evolving fiscal challenges and steps being taken to address them.

Tag: rainy day fund

Record Growth Puts Money in the Bank for California

This July marks the longest period of economic expansion in US history. For 121 months and counting, the national and state economies have experienced continuous growth.

One consequence of this sustained economic growth? An increasing stream of tax revenue flowing into the state’s treasury. This, in turn, has shaped a new state budget that contains record-breaking levels of spending.

In terms of fiscal sustainability, however, the most intriguing element of the new budget may be the dollars that weren’t spent. The budget that the legislature passed and governor just signed includes total budget reserves of more than $20 billion—also a record for the state.

The continued accumulation of budget reserves represents important progress toward preparing the state for an economic slowdown. Because of California’s tax structure, recessions hit the state’s budget particularly hard. Past recessions have caused deep drops in the level of General Fund dollars available, leading to a combination of spending cuts, tax increases, and borrowing to balance the state’s budget.

Building budget reserves should enable California to reduce the impact of a recession. Our estimates suggest that the current level of reserves would allow the state to weather the impact of a mild recession. However, they would be insufficient in the face of a moderate to severe downturn. In other words, there is still work to be done.

None of this matters if the economy never slows down. Just because the economy has gone up for so long, doesn’t mean it must fall—there is no equivalent to gravity when it comes to economics. But history suggests that recessions have a way of interrupting periods of growth. And there are some signs that clouds are gathering on the economic horizon: bond rate curves, drops in consumer confidence, and uncertainty surrounding tariffs and trade. At the same time, the stock market just finished a very positive first half of the year.

Forecasting the timing of the next recession is a much more difficult proposition than asserting that there will be one. The same could be said of California’s earthquakes. But as with earthquakes, the fact that we don’t know exactly when the next recession will hit shouldn’t stop the state from preparing for it.

K–12 Education and the New State Budget

The recently enacted 2019–20 budget allocates 28% of the total state budget for all K–12 education programs: $103.4 billion ($58.8 billion from the General Fund). Proposition 98, passed by the voters in 1988, establishes a minimum annual funding level for K–12 schools and community colleges. This year, the Proposition 98 funding level is $81.1 billion, bringing K–12 per-pupil expenditures to nearly $12,000. According to the Department of Finance, total per-pupil funding, including all federal, state, and local sources amounts to $17,423.

In addition, the rainy day fund requires the state to set aside savings for future education spending based on specific criteria, including General Fund tax revenue and Proposition 98 funding levels. This year, for the first time ever, the budget triggers a deposit into Public School System Stabilization Account at $376.5 million.

The Local Control Funding Formula (LCFF) is the primary manner in which funds are distributed to support students. This year’s budget brings the total LCFF funding to nearly $63 billion, a $1.9 billion increase from last year, accounting for a statutory cost-of-living adjustment.

This year’s enacted budget also includes funding to address a wide range of concerns, including pensions, special education, and full-day kindergarten. For teacher pensions (CalSTRS), the budget pays down the state’s ($2.9 billion) and the districts’ share ($1.6 billion) of the unfunded liability. Another $500 million for fiscal year 2019–20 reduces by 1.03% school districts’ contribution rate to CalSTRS and CalPERS (pensions for public employees). The budget adds $350 million to reduce that contribution rate by an additional 0.7% in 2020–21.

The budget aims to mitigate rising special education costs to districts by adding more than $600 million to support students with disabilities.

A $300 million one-time payment goes to the Full-Day Kindergarten Facilities Grant program, which allows districts to construct new facilities or retrofit preexisting ones for the purposes of ensuring access to full-day kindergarten.

Despite the record funding level this year, two longer-term finance issues loom. The CalSTRS funding plan, as governed by AB 1469, has set school districts’ share of teacher pension costs to increase to 18.1% in 2019–20 and to 19.1% by 2020–21. While the budget’s funding toward the districts’ contribution rate will provide much-needed relief, growing pension costs will remain challenging.

Finally, in a time of growing costs, declining student enrollment is hampering districts across the state. Over the past five years, nearly half of all districts experienced enrollment losses—and this trend may continue over the next decade. Given that the state’s funding model is based on average daily attendance, declining enrollment is likely to persist as an important fiscal issue over the long run.

Voters More Optimistic, Less Engaged

A lot has changed since Californians cast ballots just four years ago.

Likely voters today are feeling much better about the direction and economic outlook of the state. In October 2010, most (77%) said that the state was headed in the wrong direction. In our latest survey, likely voters are much more positive about the state’s future—although they are still more likely to say wrong direction (54%) than right direction (40%). Similarly, in October 2010 less than a quarter of likely voters (20%) expected good economic times in the upcoming year and far more (65%) expected bad times. Today, the mood is decidedly different, with 42% expecting good times and 47% expecting bad times. In October 2010, most likely voters (59%) named jobs and the economy as the state’s most important issue. Today, just 30% name it as the top issue, which barely keeps it in first place, while 28% name water and the drought. Further, in September 2010 nearly all likely voters (90%) called the state budget situation a big problem—today, that number is 62%.

Likely voters today are feeling much better about the direction and economic outlook of the state. In October 2010, most (77%) said that the state was headed in the wrong direction. In our latest survey, likely voters are much more positive about the state’s future—although they are still more likely to say wrong direction (54%) than right direction (40%). Similarly, in October 2010 less than a quarter of likely voters (20%) expected good economic times in the upcoming year and far more (65%) expected bad times. Today, the mood is decidedly different, with 42% expecting good times and 47% expecting bad times. In October 2010, most likely voters (59%) named jobs and the economy as the state’s most important issue. Today, just 30% name it as the top issue, which barely keeps it in first place, while 28% name water and the drought. Further, in September 2010 nearly all likely voters (90%) called the state budget situation a big problem—today, that number is 62%.

This year, likely voters are paying less attention to news about the candidates for governor than they did four years ago, when the race involved an open seat and a high-profile contest. In October 2010, an overwhelming majority were very (39%) or fairly closely (50%) paying attention to news about gubernatorial candidates. In our latest survey, just half of likely voters were doing so (18% very, 34% fairly). In addition, there is a big enthusiasm gap. Fewer voters today say they are “more enthusiastic about voting than usual” (53% 2010, 40% today).

This year, likely voters are paying less attention to news about the candidates for governor than they did four years ago, when the race involved an open seat and a high-profile contest. In October 2010, an overwhelming majority were very (39%) or fairly closely (50%) paying attention to news about gubernatorial candidates. In our latest survey, just half of likely voters were doing so (18% very, 34% fairly). In addition, there is a big enthusiasm gap. Fewer voters today say they are “more enthusiastic about voting than usual” (53% 2010, 40% today).

In 2010, when many people were tuned into the top of the ticket race, nearly 60 percent of registered voters turned out to vote. With far fewer voters paying attention to the gubernatorial race—and with the lack of a Congressional senate race—what can we expect in 2014? Will concerns about the drought and the state budget drive people to the polls—and if so, how will this translate into votes on Proposition 1, the water bond, and Proposition 2, the establishment of a rainy day fund? Stay tuned to PPIC as we continue to follow the November 2014 election.